RHM/RCC RESULTS AS OF 5/8/235/7/2023 In my Opinion, As an Elected Supervisor of Exeter Township:  The CPA for the township provides a valuable service, they are responsible for assuring and forming an opinion on our financial statements (prepared by our employees) that they can be relied on because they are formulated following GAAP: Generally Accepted Accounting Principles. I am a CMA, (Certified Management Accountant) I am trained and experienced in evaluating the financial information contained in the financial information of the township. I look at it from a business/operations point of view which can differ significantly from GAAP requirements. You will often hear the term"NON GAAP" used indicating deviating from the GAAP. This often is the case when you evaluate the results. This is not audited financial information. It is compiled from financial information obtained from township documents available to the general public. Let's look at the information I am providing you above. It represents all the information currently available to you and myself. (public record) The top portion are all the amounts our FUND 10 ( The clubhouse fund) has received since the beginning of our arrangement with RHM LLC. It includes the amount they will transfer this Monday 5.8.23 and you can see since inception we, the TAXPAYERS have received $38,451.68. You can see I have provided the source of this information, it is public and you can find it on EXETER TWP website. The next section are the amounts that we have paid to RHM LLC, $172,831.73, 4.5 times the amount the TAXPAYER received. I provide the source of this information just as I have for the amounts we received. (our %). The. source of this information is the check runs also referred to as the check distribution which is part of every meeting. I have provided the date of each check run and the total of all the invoices listed in that check run. You can find this report by going to the AGENDA for the particular meeting and you will find it listed as one of the reports. As you can see, including the amount we will approve to pay RHM LLC on May 8, 2023 ($58,307.61) the total since our agreement with RHM LLC is $172,831.73. The last line on this report is the total amount of cash that has flowed into our municipal accounting process (does not include sales tax, a later discussion on this will follow) The total cash flow from all of the amount from October 2022 thru April of 2023 is $211,283.41. (7 months) This amount is the addition of the money shared with you (the taxpayer) $38,451.68 plus the amount you paid RHM LLC in the amount of $172,831.73. This is everything. that is recorded on our municipalities BOOKS. You can see for yourself in the far right column the percentage of participation in the cash coming thru our RCC EVENT account. It is clear, at least to me, that we are receiving only 18% on average.THEY GET 82%! You will hear excuses for this but don't believe them. The taxpayer( represented by the Supervisors) have struck a terrible deal and in my opinion (all of this is my opinion by the way). YOU DECIDE SINCE YOUR TAXES ARE SUBSIDIZING THE RCC TO THE TUNE OF APPROXIMATELY $1,500,000 ANNUALLY.

0 Comments

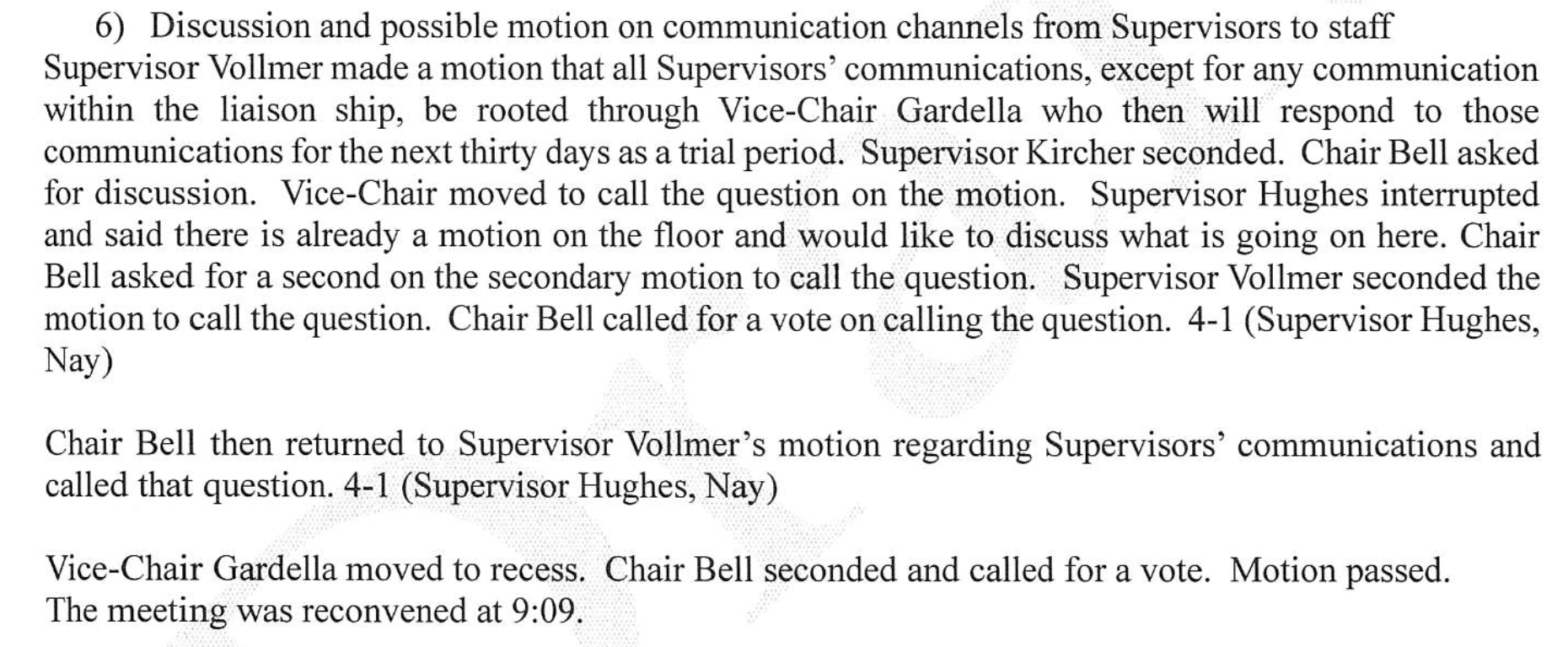

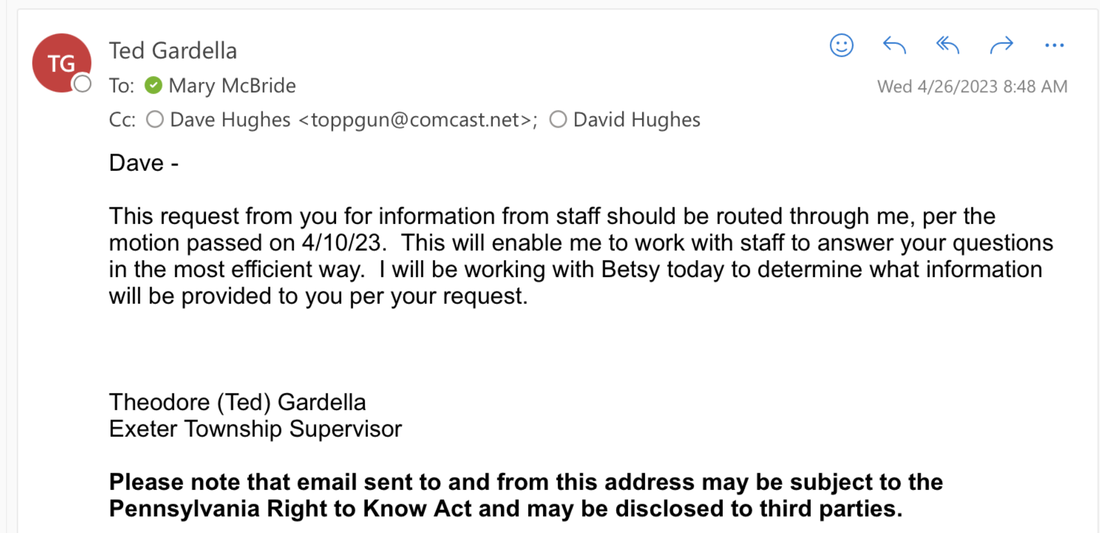

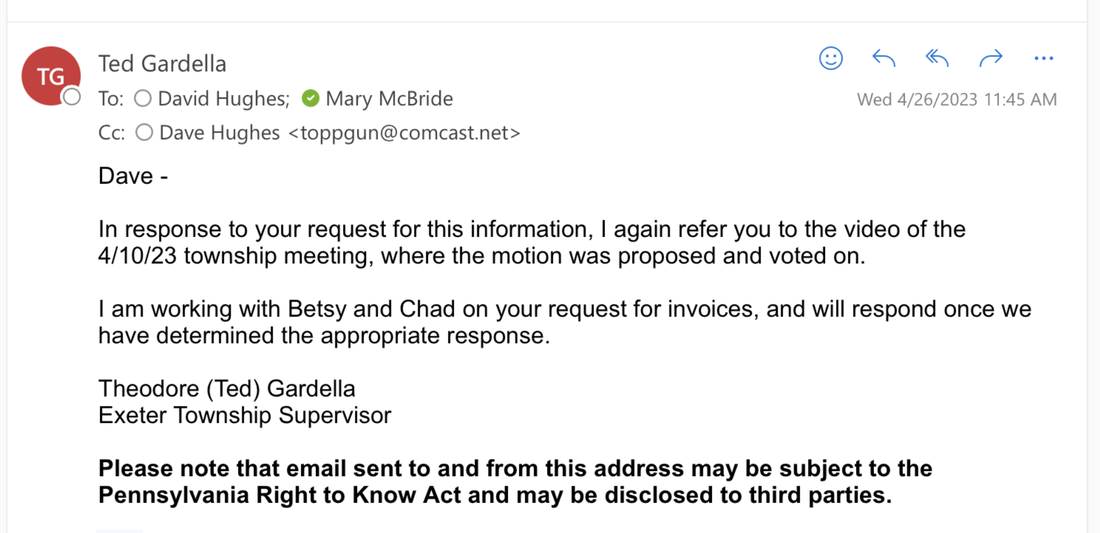

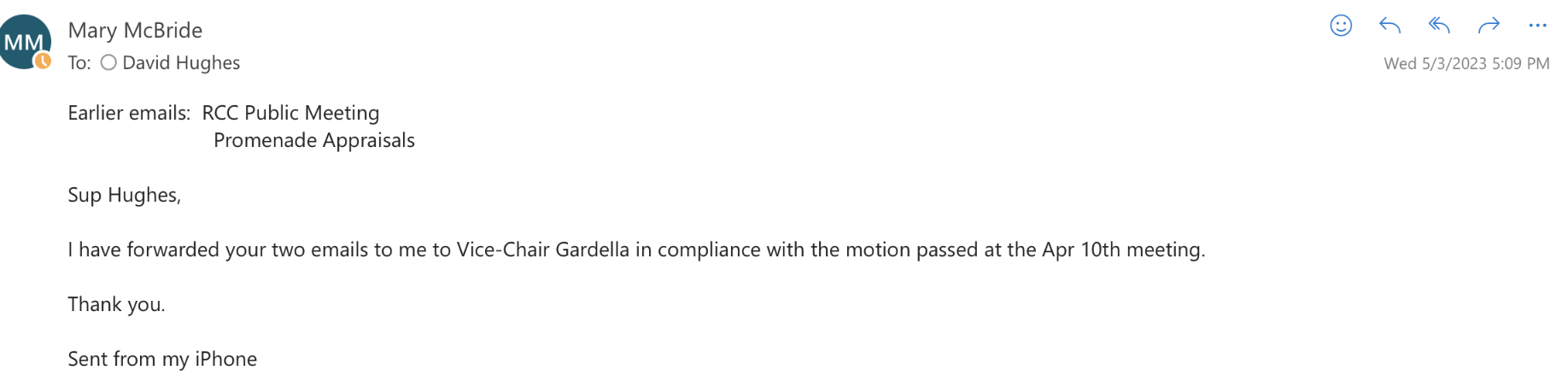

1. On MAY 8, 2023 the Board of Supervisors will deliberate extending a requirement where I have had to route all communications and requests for information to another supervisor (instead of requesting from the manager or department heads directly) They decided that all communications (except for those who call themselves liaisons) must be routed through Supervisor TED GARDELLA. Below are examples of what happened with my requests for information that I felt I needed to do mt job properly:  2. On April 10, 2023 the four supervisors passed this motion. The only supervisor who was not a liaison, you guessed it, ME. PLEASE NOTE: the motion is about ROUTING -- has nothing to do with allowing or denying access, It says nothing about Supervisor Gardella approving or denying access to information necessary for any supervisor to do the job they were elected for, yet THIS IS WHAT GARDELLA DOES: DENY ACCESS and of course uses phony irrelevant reasons. Read closely the following correspondence :

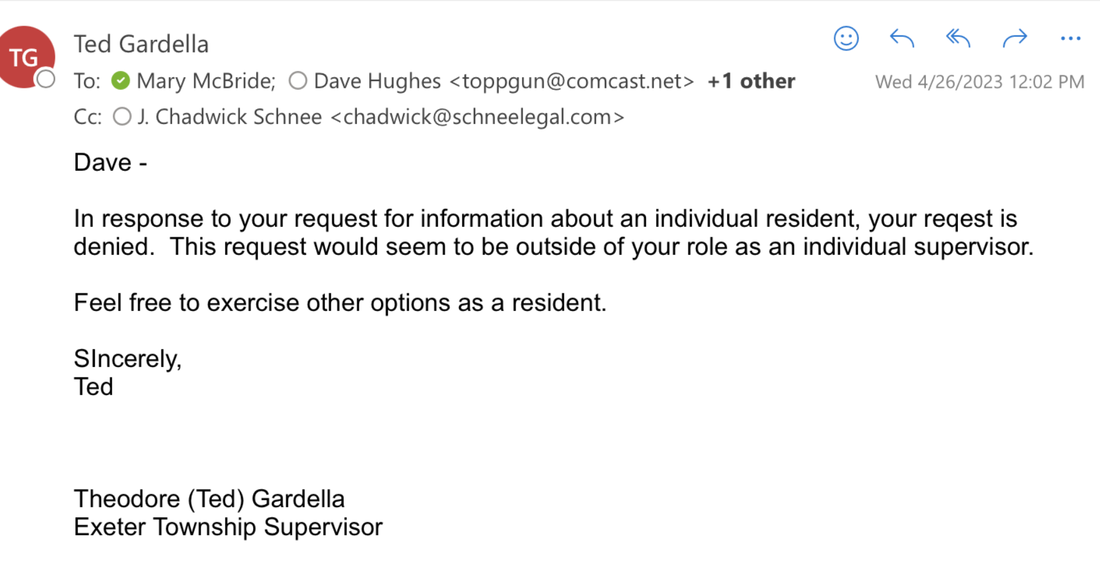

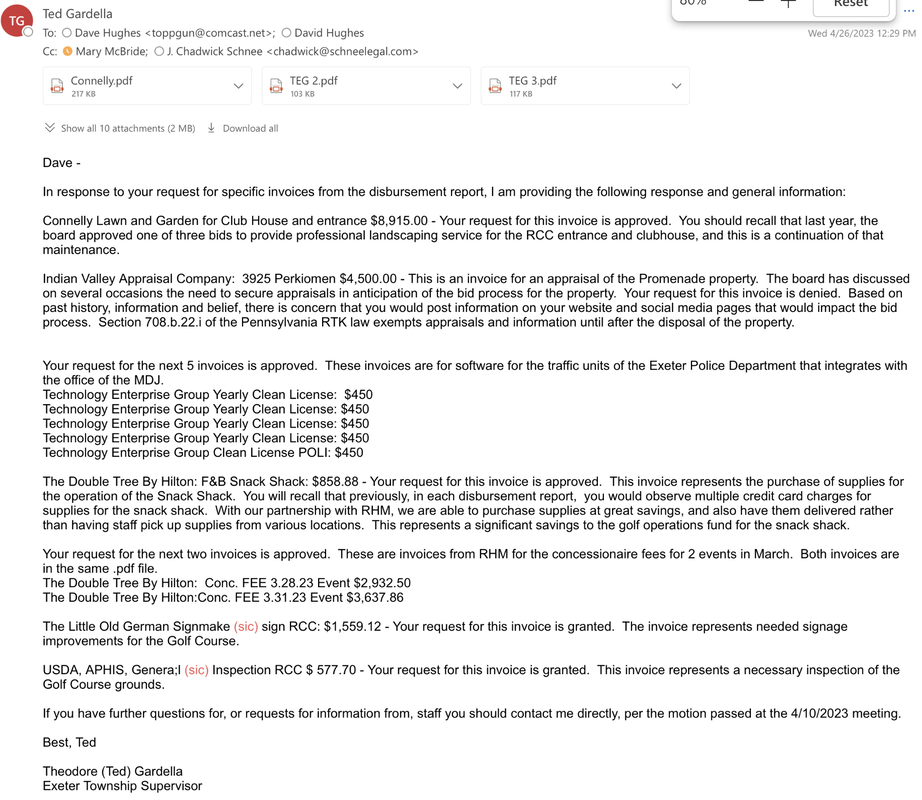

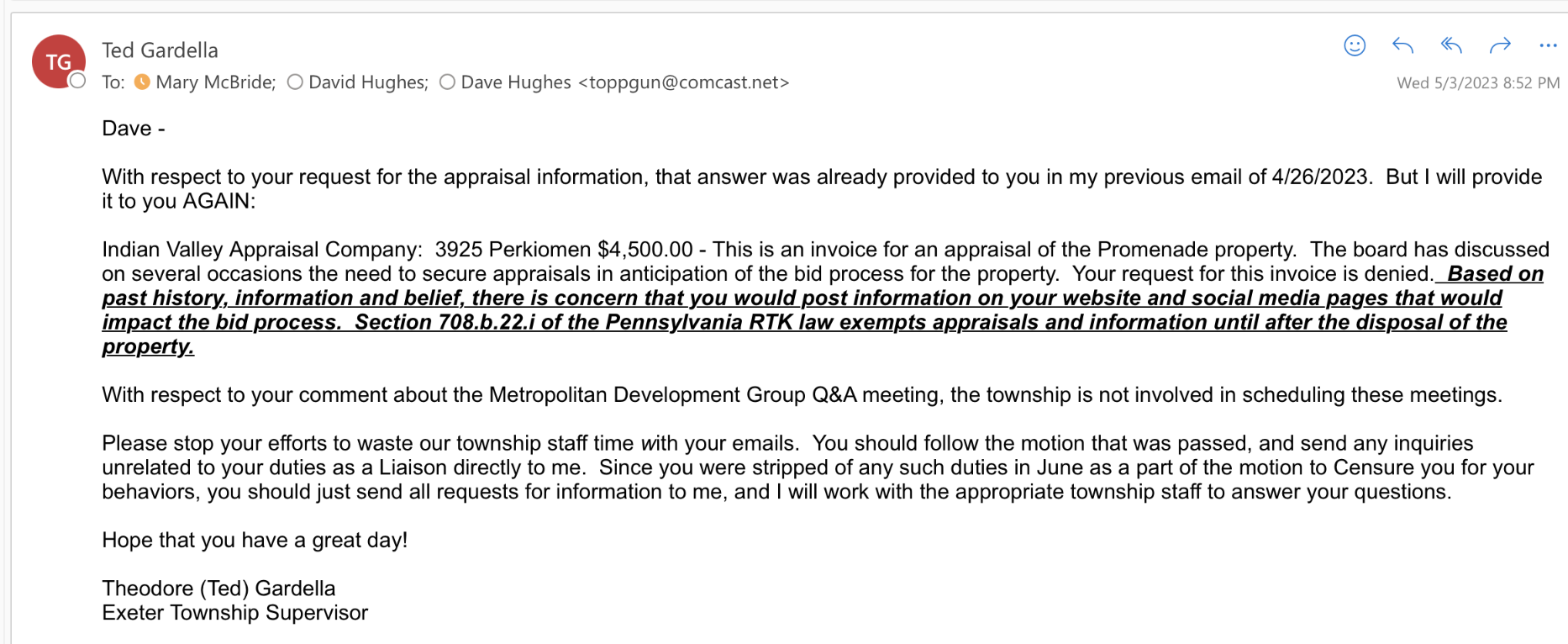

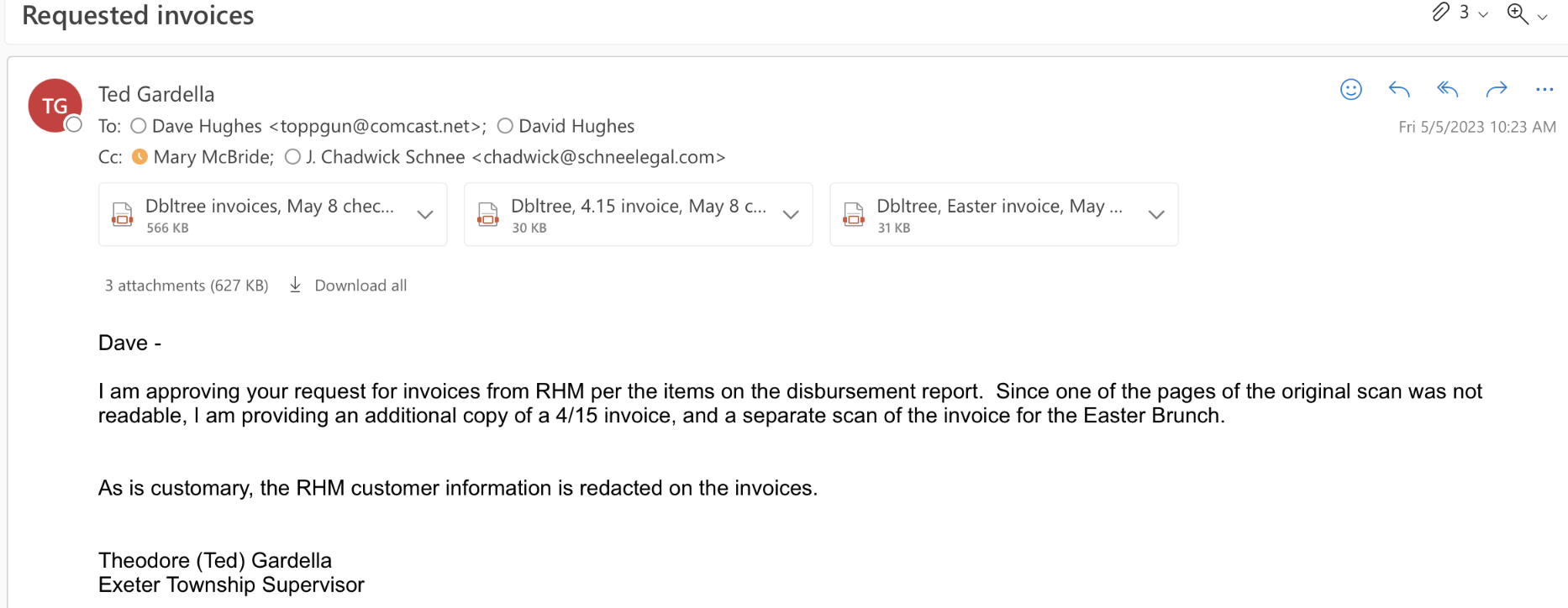

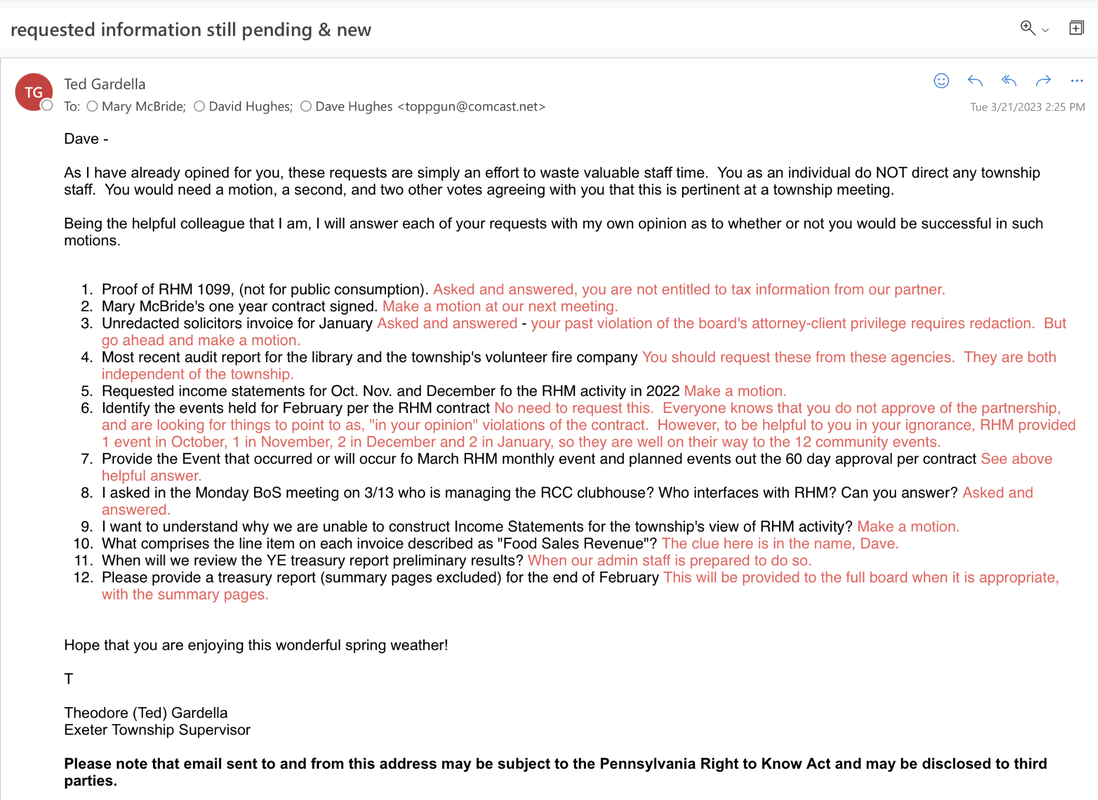

My request was not for any document, it was related to a supervisor who has indicated on his SOFI (Statement of Financial Interests, a required legal document that all supervisors must report every year) that he conducts four businesses out of his residence. I asked verification, no documents, just a verification that permits exist for the supervisor to conduct these businesses in a residential area. One business is the manufacture and sale of guns.  Note: reference to the 4.10.23 motion and I must contact TED GARDELLA directly. A supervisor controlling what another supervisor can see or do. All perpetrated by Bell and Vollmer.  Proof of the Township managers compliance and refusal to provide requested information to a supervisor.  Information was not provided, I asked for the Appraisal values obtained from the appraisal...   Most recent for the 5.8.23 BOS meeting please note invoices for RHM are redacted.  The RED are comments from TED GARDELLA ABUSE OF POWER IS A FELONY, In time we shall see whether Gardella, Bell and Vollmer's qualified immunity stands in front of that ... or not ..... The above blog and analysis is solely based on my opinion.

Let's ChatCategories

All

Archives

July 2023

|